China, bitcoin and operations are key focus while pandemic and political risks top concerns

16 March 2021

By Will Acworth

FIA conducted a survey at the beginning of 2021 to assess the outlook for the global cleared derivatives industry. The survey gathered feedback from people working at banks, brokers, exchanges, technology vendors and other firms that support the trading and clearing of derivatives such as futures and options.

Download the full survey results.

The purpose of the survey was to gauge sentiment in four areas:

- The outlook for trading activity, profitability and competition over the next 12 months.

- Current political, regulatory and technology issues facing the industry.

- The degree of interest in two emerging areas of growth — China and bitcoin.

- The need for modernization and innovation in the trading and clearing workflow.

FIA conducted the survey during January and February. Responses were collected on an anonymous basis. A total of 274 responses were received, with 57% from the Americas, 31% from Europe and the Middle East, and 12% from the APAC region.

The responses came primarily from firms that are directly involved in supporting the infrastructure of the global cleared derivatives markets, with 22% from exchanges and clearinghouses, 34% from banks and brokers that serve as intermediaries for customers accessing these markets, 22% from technology vendors and service providers, and 14% from asset managers, commodity suppliers and proprietary trading firms.

The intermediary category includes three types of firms: banks that provide trading and clearing services for their customers, non-bank firms that provide trading and clearing services, and brokers that provide execution services only.

Main findings:

- Optimism on volume: The survey found that two-thirds of respondents expect trading volume, one of the main drivers for growth in this industry, to continue rising in 2021. Derivatives based on commodities and equities, both of which set records for the number of contracts traded in 2020, are seen as the areas with the highest potential for growth.

- Pandemic concerns: The survey also found deep concern about the pandemic’s impact, with half of respondents ranking it as the top concern facing the industry this year. Political risk came in second on the list of concerns, followed by technology disruption. Capital requirements, one of the biggest concerns for many firms after the financial crisis, ranked fourth.

- Brexit challenges: The survey found that Brexit is viewed primarily as a regulatory challenge. Relatively few people expressed concern about its potential to disrupt derivatives markets, which may reflect the fact that many firms have already relocated staffing and reoriented their systems. Instead, the respondents flagged the potential for regulatory conflicts and compliance issues as a more critical problem for the industry, given that many firms will need to comply with both UK and EU rules in order to continue serving their customers.

- China opportunities: The survey also assessed the industry’s level of engagement with the Chinese futures markets, which are among the largest and fastest growing in the world. Access to these markets is limited, but 24% of the respondents reported that their firms are already actively participating, and another 9% said that their firms are likely to enter by the end of this year.

- Digital assets: The survey found a similar level of engagement with digital assets. Among respondents, 31% said their firms are already participating in markets for bitcoin and other digital assets, and another 10% said their firms are likely to enter by the end of this year. The responses showed a marked split by type of firm, however. Exchanges, independent brokers and technology vendors were the most engaged with this new asset class, while banks and asset managers tended to be “watching with interest” from the sidelines.

- Technology trends: Looking inward at the industry’s use of technology, respondents pointed to several areas in the trading and clearing process where innovation and modernization are needed. Post-trade processing was at the top of the list, followed by regulatory compliance and then risk management and collateral management tied for third.

Outlook for trading volume

The survey asked for feedback on expectations for trading volumes in derivatives markets over the next 12 months. Results showed 66% of the respondents said they expect trading volumes to increase, 23% said they would stay the same, and 11% said they would decrease.

Breaking down responses by type of firm, bank-owned clearing firms were not as optimistic as other segments of the industry. Only 44% of respondents working at bank-owned clearing firms thought volumes would increase, compared to 76% of respondents working at independent clearing firms and 71% of respondents working at exchanges and clearinghouses.

Regionally, respondents in the Asia Pacific region and the Americas were more confident of growing volumes over the next 12 months, with 72% and 70% expecting an increase, respectively. In contrast, only 56% of the respondents in the EMEA region expected trading volume to increase.

When asked which region has the greatest potential for growth, 45% of all respondents said Asia Pacific and 36% said the US. This finding is in-line with recent trends in trading activity. In 2020, the total number of contracts traded on exchanges in the Asia Pacific region jumped 39% from the previous year, with exchanges in China and India accounting for most of that increase. Meanwhile, trading on North American exchanges rose 25% from the previous year, with a surge in retail trading of equity futures and options offsetting a decline in the trading of interest rate contracts.

Not surprisingly, respondents in Asia Pacific were the most optimistic about that region, with 82% seeing APAC as having the highest potential for growth over the next 12 months. On the other hand, respondents in the Americas were more split, with 49% favoring the US and 36% favoring APAC. The EMEA region’s participants were the most evenly balanced in their views, with 45% favoring APAC, 23% EMEA and 22% the US.

When asked which asset classes have the greatest potential for growth, 33% of all respondents said derivatives based on commodities and 27% said equities. These two categories both set records in 2020 for the annual number of contracts traded. In addition, these two categories are likely to gain as economic activity returns to normal over the course of 2021.

Breaking the asset class responses down by type of firm, respondents working at exchanges and clearinghouses saw equal potential for growth in commodities and equities. Clearing firms, on the other hand, were split. Bank-owned clearing firms were more optimistic about equities, while independent clearing firms were more optimistic about commodities. This may reflect differences in their client bases; asset managers that use equity futures and options as investment tools typically use bank-owned clearing firms, while companies involved in the production and processing of commodities often rely on independent clearing firms.

The survey also asked for views on other growth trends. The survey found that industry professionals generally are optimistic about the outlook for profitability at their firms, with 61% expecting it to rise over the next 12 months and only 12% expecting it to decrease. On the other hand, most people expect the level of competition to intensify. When asked about the competition that their firms face in the derivatives markets, 53% said they expect competition to increase over the next 12 months, 34% said they expect it to stay the same, and only 13% said they expect it to decrease.

Industry Issues

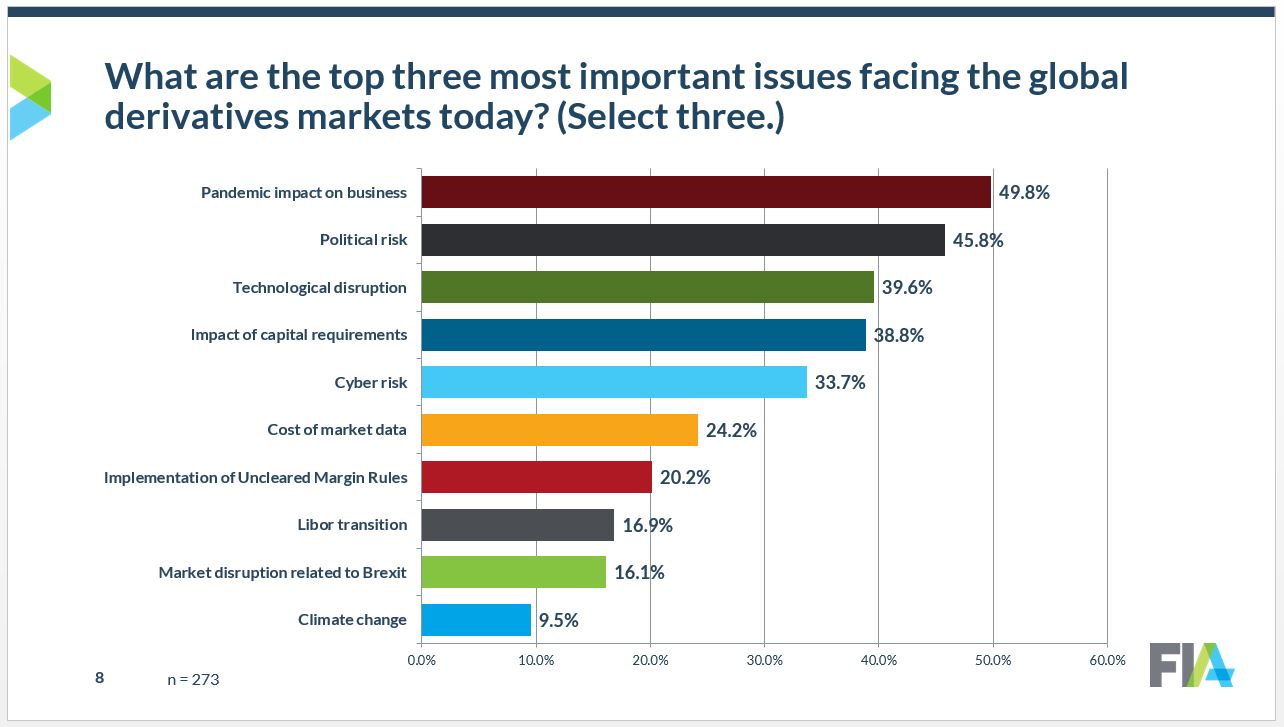

The FIA survey asked respondents to name the top three most important issues currently facing the global markets.

The most cited issue was the pandemic’s impact on business. Although the derivatives markets were able to continue operating during the pandemic without significant disruption, the health of these markets is closely tied to the level of economic activity. Many institutional investors pulled back from trading derivatives during 2020, particularly interest rate derivatives, and commercial hedging was curtailed in several important commodity markets.

Second on the list was political risk, a sign that many industry professionals are worried about the potential impact of new legislation and regulation. This is especially true in the US, which at the time of the survey was undergoing a transition to a new administration. It also may reflect ongoing concerns about economic disputes between the US and China, which have led to new restrictions on certain types of cross-border trading.

Third on the list was technological disruption. Although this issue is not new, several recent developments have brought it to the fore, notably the emergence of new forms of retail trading, rapid advances in the use of the cloud, and greater use of artificial intelligence in many parts of the trading lifecycle.

Drilling down to responses by type of firm, respondents working at bank-owned clearing firms listed capital requirements as their top concern, ahead of the pandemic, political risk and technological disruption. This reflects the impact of the Basel III capital requirements on the cost of providing clearing services to clients. These requirements apply only to banks, but they also have an indirect effect on clients by reducing the capacity of bank-owned clearing firms to take on more risk. That helps explain why market-making firms, many of which rely on banks to clear their trades, cited capital requirements as the second-most important issue facing the industry after political risk.

The survey also revealed several insights on the impact of Brexit. Only 16% of the respondents cited market disruptions related to Brexit as one of the top three issues facing the industry. This may reflect the fact that at the time the survey was conducted, many firms had already relocated staffing and reoriented their trading and clearing systems in anticipation of the UK’s departure from the European Union.

Instead, the respondents flagged the potential for regulatory conflicts and compliance issues as a more critical problem for the industry, given that many firms will need to comply with both UK and EU rules in order to continue serving their customers. When asked to identify their top concern about the impact of Brexit on the derivatives industry, 51% said regulatory conflicts and compliance costs, 23% said market fragmentation, and 19% said higher costs to run their businesses.

The survey revealed significant concerns about two other issues facing the industry — cyber risk and market data. Roughly one third of all respondents ranked cyber risk as one of the top three issues facing the industry, a sign that people in the derivatives industry are worried about the risk that cyber criminals will penetrate networks, access confidential files, and disrupt markets. Another 24% included the cost of market data in their list of the top three issues facing the industry. Market data is essential to trading and clearing operations, and the exchanges that produce these data derive a large and growing part of their revenues from the sale of these data. That is leading to friction between market participants and the exchanges over the cost of these data.

Emerging opportunities – derivatives industry

The survey included several questions to gauge industry sentiment around emerging business opportunities in two areas: the rapidly growing futures markets in China, and the emerging markets for digital assets such as bitcoin.

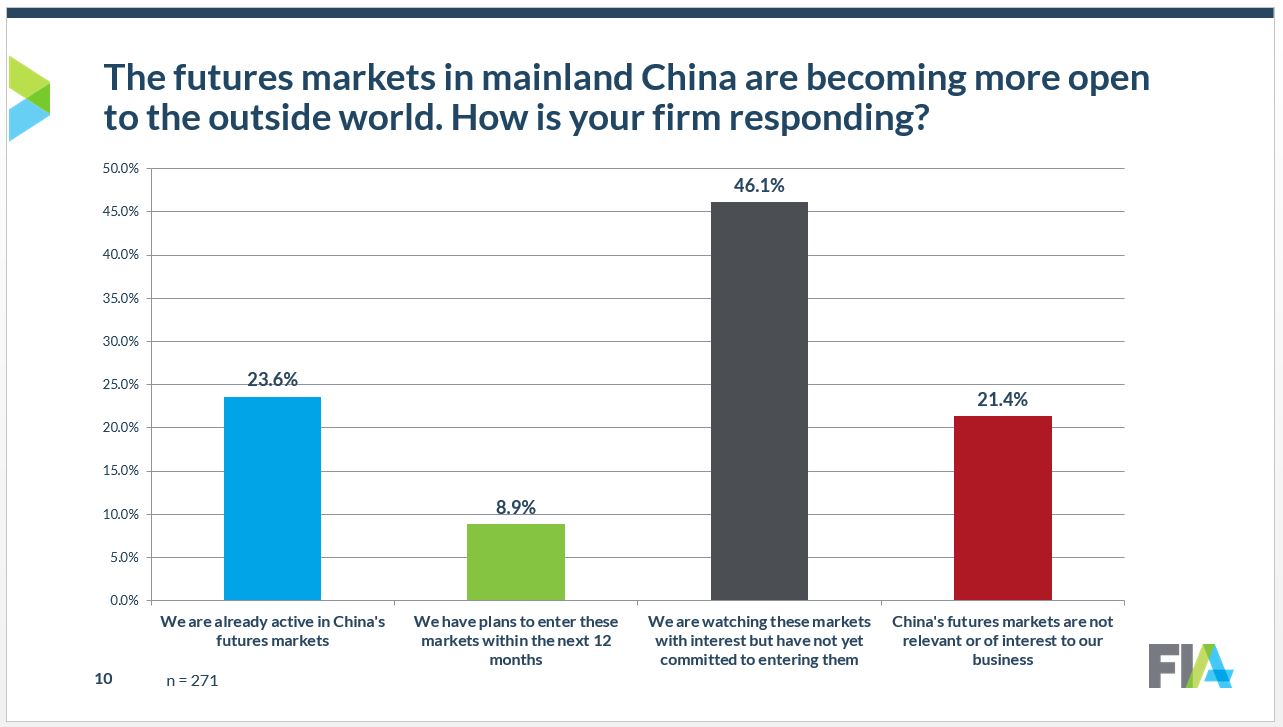

The survey asked how firms are responding to the gradual liberalization of access to the futures markets in mainland China. Among respondents, 24% said their firms are already active in these markets. Another 9% said their firms plan to enter in the next 12 months. 46% said their firms are “watching with interest” but have not yet decided to enter, and 21% said China’s futures markets are not relevant to their firms.

Breaking this down by type of firm revealed important differences. Two thirds of the respondents working at commodity firms said their firms are already active in China’s futures markets, more than any other segment of the industry. Asset managers, on the other hand, are mainly watching with interest but have not yet committed to entering these markets. Among intermediaries, 44% of the people working at clearing firms, both bank and non-bank, said their firms are already active in these markets, and another 7% said they expect to enter in the next 12 months.

Turning to digital assets, the survey revealed a very similar level of interest among respondents. 31% said their firms are already active in digital asset markets, and 10% plan to enter these markets in the next 12 months. The level of engagement was highest with independent clearing firms and technology vendors, with 44% and 43% of respondents, respectively, saying their firms are already active. Bank-owned clearing firms, on the other hand, are much less engaged, with only 29% saying that their firms are active currently and none saying that their firms plan to enter these markets in the next 12 months.

The survey also asked respondents for their views on the regulation of digital assets. Uncertainty around this issue has been one of the main obstacles to greater involvement by firms in the derivatives industry. 40% said policymakers should clarify regulatory jurisdiction and oversight of these products and write new rules accordingly. 37% said regulators should treat these assets like other financial instruments and enforce compliance of existing rules and regulations. 17% called for the industry to set its own standards and regulate itself. Only 6% called for a laissez faire “do no harm” approach and allowing this sector to develop without regulation.

Part 4: Modernization and Innovation

One of the key lessons that the derivatives industry learned from the pandemic is that the burst in trading volume that took place during March put a heavy burden on operational capacity, leading to delays in the settlement of trades. The experience highlighted the need for more investment in the technologies used to process trades after execution.

To gather more information about this trend, the survey asked respondents to identify the areas in the trading and clearing process that are most in need of innovation and modernization.

Post-trade processing was at the top of the list, reflecting the awareness in the industry that legacy technology has become a significant obstacle to the efficient processing of trades. Although the vast majority of trades are processing on a straight-through basis, a small number require manual intervention to correct errors and allocate positions properly.

Regulatory compliance came in second. In recent years, reporting requirements have increased in complexity, making it more important than ever to gather data efficiently. In addition, the explosion of trading volume has intensified the need for advanced tools to sift through millions of transaction records.

Two areas tied for third — risk management and collateral management. Risk management refers to the systems that firms use to monitor risks in trading. Although some firms have developed systems to manage risks on a near-real-time basis, this area continues to be a challenge for the industry. Collateral management refers to the movement of cash and securities to meet margin requirements. Some firms have begun transforming key elements of this process through the use of cloud computing and distributed ledger technology, but this trend is still in its infancy.